Sustainability Reports for Business: how to prepare for the unexpected?

Sustainability has become a popular topic in all industries. Investors are also paying close attention to this issue, requiring companies to provide adequate and relevant information on their sustainability performance before making investment decisions.

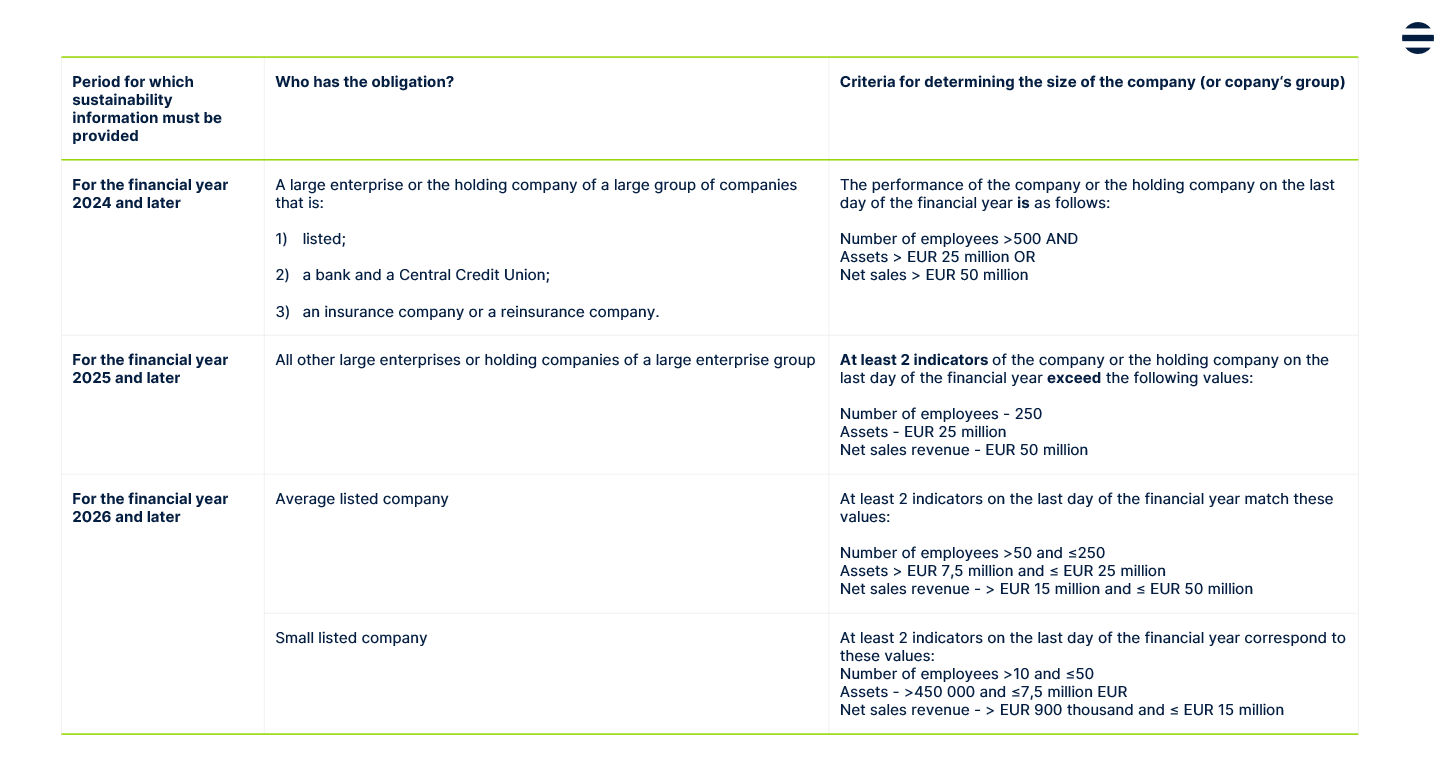

Lithuania, like other EU countries, has started to implement Directive (EU) 2022/2464 of the European Parliament and of the Council, which aims to regulate companies’ provision of sustainability information. From next year onwards, this topic will become relevant for a significant number of companies. If a company has assets of more than €25 million, or sales revenues of more than €50 million, or has more than 250 employees – two of the three requirements – will require the preparation and submission of sustainability reports. Rūta Armonė, Partner at Ellex Valiunas, and Aušra Abraitytė-Gedminė, Associate at Ellex Valiunas, share their insights on this matter.

Main innovations introduced by the new regulation

Sustainability reporting becomes mandatory for companies

Under the previous regulation, companies established in Lithuania and listed on the Lithuanian or international stock exchanges were obligated to report on a specific degree of social responsibility.

However, starting 2025, non-listed companies whose assets at the end of the financial year exceed EUR 25 million, or whose sales revenues exceed EUR 50 million, or whose number of employees exceeds 250 will be required to submit sustainability reports as well – you only need to meet 2 of the above criteria to be obliged to prepare and publish sustainability reports.

Sustainability reporting will involve more and more companies each year:

Sustainability information will need to cover not only information about the company’s/group’s activities, but also its value chain, including products and services, business relationships and even the supply chain.

Given the broad concept of sustainability information, if a company does not have all the information it needs to provide on its value chain, for the first 3 years it will be able to state it in its management report. It will also need to explain what efforts are being made to obtain the required information, as well as the reasons why all the required information has not been obtained and the plans for obtaining it in the future.

The company’s set of annual financial statements, together with the management report, as well as the sustainability report (where the management report is required by law to include information on sustainability issues), must be submitted to the Register of Legal Entities within 30 days of the ordinary general meeting of shareholders and published on the company’s website.

The annual report is replaced by the management report

The annual report, so familiar to companies, is changing its name and is now called the management report.

The management report will continue to form part of the company’s annual set of financial statements and will include the following information:

- General data;

- Corporate Governance Report;

- Remuneration report;

- Sustainability Report.

Of course, individual elements of the management report are not mandatory for all companies. As in the past, the legislation provides for slightly adjusted criteria for deciding the extent to which a management report is necessary for a particular company.

Impact on business

The package of legislative changes is said to be an attempt to reduce administrative burdens by removing redundant requirements and unclear regulation. However, the implementation of the Directive does not take any account of the industries in which companies operate. Regardless of whether a company is in the manufacturing industry or in the technology sector, additional costs will have to be incurred for the collection of sustainability information and the preparation of the report.

A new obligation of sustainability accountability also comes into force, which will further increase companies’ spending on sustainability issues. Sustainability information will have to be assured by a third party outside the company. The service of sustainability reporting assurance will primarily be provided by independent sustainability reporting specialists and, as in the case of financial audits, can be offered by auditors and audit firms. The person or firm performing the assurance will have to be approved by a shareholder resolution.

Taking these considerations into account, the turnover and other criteria set out in the legislation could have been higher, targeting genuinely large companies or groups of companies.

Ignoring the obligation to produce sustainability reports – brings consequences

As is common for breaches of corporate law, failure to comply with the obligation imposes administrative liability on company executives. This can range between €600 and €1,450, and €2,000 to €6,000 in the case of repeated violations.

How can we prepare ourselves so that the obligation of sustainability doesn’t take us by surprise?

Management should focus on the following matters when preparing the sustainability report:

- who in the company is/will be responsible for sustainability issues;

- what sustainability projects and measures the company has / will have in place;

- what sustainability-related policies, processes and procedures the company already has in place and what is still missing;

- whether the expertise of existing staff is sufficient to fulfil the sustainability function, or whether external legal/sustainability advisors are needed;

- how sustainability-related information will be collected and where and in what form it will be collected;

- who will be responsible for preparing the sustainability report and how much this may cost the company.

And to be fully prepared for the implementation of sustainability obligations, it should be remembered that the sustainability assessment will have to apply a double materiality model. This essentially means that in the context of sustainability, we will need to look not only at the environmental and societal impacts of the company’s activities, but also at the risks and opportunities that sustainability challenges (e.g. climate change) may present to the company.

In this regard, management should plan to use external advisors to help identify areas of sustainability relevance to the company by assessing the company’s performance from the outside.

Linked Services